Via Baker & Company Advisory Group,

- The U.S. economy is not as solid as it appears.

- Statistical anomalies hide profound weakness.

- I will examine actual GDP and actual employment.

- Warning: not for the faint of heart.

Do you consider debt as income? Before you answer that, let’s perform a thought experiment. Imagine that you had taken a long cruise last fall and charged $10,000 to an American Express card. When you did your taxes this year, would have told the IRS that you had $10,000 income from American Express? Of course you wouldn’t. Suppose a major oil company issues $800 million worth of bonds to develop a new old field. Would the company report that as income to the stockholders or the IRS? Of course they wouldn’t. I am sure those sound like silly questions as the answer is a self evident “NO!” We do not consider borrowed money as income. It is a liability that must be paid back. Then why do we count Federal Government debt when measuring national income? I will leave speculation as to the “why” to the readers and focus on the fact that we do count new Treasury Debt as income.

The modern concept of GDP was first developed by the Department of Commerce in 1934. Commerce commissioned Nobel Laureate Simon Kuznets of the National Bureau of Economic Research to develop a set of national economic accounts. Professor Kuznets headed a small group within the Bureau of Foreign and Domestic Commerce’s Division of Economic Research. I picture them meeting to develop statistical measures that would help the government to determine if the economy was recovering from the Depression. They are debating on how to measure all of the various sources of income. One economist suggests that regardless of the source of his income, there are only two things he can do… Spend it or invest it and we know how to measure consumption and investment (& savings). This was the foundation of the expenditure approach to measure GDP. I can imagine another one of the economists suggesting that when we sell more to other countries, the excess should be added to national income and subtracted if we buy more than we sell (Balance of Trade). Then another economist suggests that there is a third alternative to the idea that he will either spend or invest his income and that is paying taxes. Since the government takes a portion of National Income and spends it, they decided to add Government spending into the GDP calculations. While each component of this basic formula for GDP breaks down into hundreds or thousands of sub-components, the final calculation is:

GDP= PI + BT + GS

Where PI is private income (measured as consumption or investment)

Where BT is balance of trade

Where GS is government spending

So the final formula for GDP includes Government Spending. Notice that the government spending component does not take into account whether or not the government spent money taken out of private income (taxes) or borrowed it. When measuring National Income, we are giving equal weight to spending taxes on actual Private Income and money the Treasury borrows.

I suggest that government debt is not part of “ National Income” because it is not income. It is borrowed (often from sovereigns that are not our friends) and must be paid back eventually. We do not consider borrowed money as income anywhere else and it shouldn’t be considered as National Income. Debt is artificial stimulus not National Income! Governments must pay back debt either through higher taxes, inflation/depreciated currency, reduced services or some combination thereof. If we want an accurate picture of whether or not the economy is self sustaining, then we need to consider a measure I would like to introduce as “Actual National Income”which does not count artificial stimulus. Therefore to accurately measure the health of the economy, government debt must be subtracted from the formula. Please consider the GDP formula with the following modification.

Actual GDP = PI + BT + (GS – GB)

Where GB is government borrowing

So, if you acknowledge for the sake of argument that government debt is not actual national income, the following graph is how the U.S. economy looks like excluding stimulus. This is Actual GDP excluding artificial stimulus.

The data and chart comes from the Federal Reserve Economic Data base (FRED.) It is Gross domestic Product minus Treasury Debt. If you download them to a spread sheet GDP is expressed in billions so 1,000,000,000 is expressed as 1, while Federal Debt is expressed in millions so 1,000,000,000 is expressed as 1,000. That is why the chart is (Gross Domestic Product * 1000.)

The government has always borrowed and spent money but actual GDP has grown as far back as the Fed has data. That is until 2008. Then something in our economy broke. Since then it appears the economy has been in what would be considered a depression but masked by huge Federal Government stimulus borrowing. Have we reached a level of economic activity that could sustain itself without this artificial stimulus? What would happen if the Government was forced to balance the budget? You decide for yourself, but remember that would remove 5-7% of our GDP. An economic depression is generally defined as a severe downturn that lasts several years. Does this look like a severe downturn that is still lasting several years? This is what our GDP minus artificial stimulus looks like.

Does that chart look like the data on a self sustaining recovery? If it were self sustaining the slope would be rising as it was prior to 2008. It continues to decline and is therefore anything but self-sustaining. In economics, deficit spending has long been called “Fiscal Stimulus.” Since 2008, this artificial stimulus has averaged 7.45% of GDP. The arithmetic (GDP-GB) is quite simple; without the artificial stimulus created by spending the proceeds of newly issued Treasury bonds, our GDP has declined an average of 7.45% each year since 2007! The following data/proof is downloaded from the source of the previous chart.

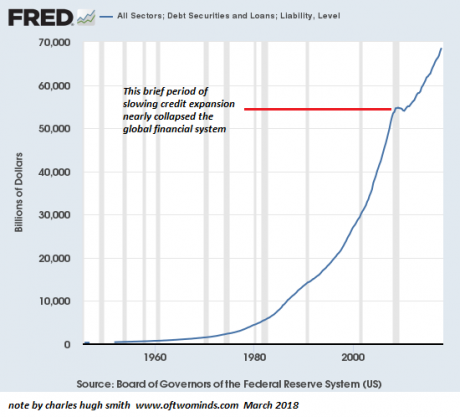

From 1929 to the end of the Great Depression and WWII, the Fed increased its balance sheet from 6% of GDP to 16% of GDP. From 2008 to 2014 the Fed grew its balance sheet from 6% of GDP to over 22% of GDP. The effective FED Funds target rate sank to 0-¼% band at the end of 2008 and stayed there until the end of 2015, when they went to 1/4-1/2% and stayed there a year. In fact, the Fed did not start serially raising rates until the end of 2016. Essentially, the Fed sat at the zero boundary for 8 years. Many wonder why they took so long to start the process of normalizing rates.

The FED has given us 8 years of “0” rates and almost twice as much of an increase in balance sheet expansion as they used in the Great Depression and WWII. Why? Did they see something that was more dangerous than the dual threats to the U.S.’s actual existence than the Great Depression and WWII combined? Or perhaps they were just engaged in a reckless and potentially dangerous monetary experiment? I have been asking those questions since the Fed’s balance sheet expansion exceeded that of the Great Depression & WWII. I believe what I have been describing as “ Actual GDP” may provide the answer. The Fed & the Government may have seen a depression that had the potential to be more threatening, deeper and longer than that of the 1930’s. If that assumption is correct, then the Fed & the Government have successfully masked a depression, avoiding a negative feedback loop and giving the economy time to heal. Has it healed? Please refer to the first graph “GDP minus Federal Debt” chart and tell me if you think the actual economy has healed. It is still heading down so I believe an informed and rational answer would be NO. If it has not healed one wonders what the Fed is doing.

In a report published on Wednesday August 30, 2017, titled “With A Shutdown, There Will Be Blood”, U.S. chief economist at S&P, Beth Ann Bovino, writes that “failure to raise the debt limit would likely be more catastrophic to the economy than the 2008 failure of Lehman Brothers and would erase any of the gains of the subsequent recovery.” I believe Bivino is on to something, even though we now have a temporary extension of the debt ceiling. With the Federal Government borrowing and spending over 6-7% of GDP, then it stands to reason that without the Government’s ability to borrow new money, GDP would collapse 6-7% before a negative feedback loop type mechanism is engaged making it worse. It is just arithmetic. Since 2010 the amount of net new Treasury Bonds issued has averaged 6.5% of GDP. If the Federal Government were unable to issue new bonds then that amount would no longer be in GDP. Again, It is just arithmetic.

The labor market is reported as having created millions of jobs, but what kind of jobs? We often hear that we have full employment and a very tight labor market, that we have created so many jobs the Fed must raise rates. Since no one wants to raise a family working multiple part time jobs, let’s examine U.S. employment in terms of full time jobs,

The Federal Reserve data base (drawing on U.S. Bureau of Labor Statics) tells us there were 121,875,000 people employed with full time jobs in November of 2007 (just before the 2008 crises). As of August 2017 there were 125,755,000 people with full time jobs. That means our economy has added a paltry 3,880,000 full time jobs in almost 10 years as the population grew by about 23 million.

According to the National Center for Educational statistics there were 3,897,000 people who received a college degree including associates, bachelors, masters and PHDs in the school year 2016-2017.

The good news is that most of the people who graduated from college in the 2016/2017 school year can have full time jobs. The bad news is that in the 2016/2017 school year, those who dropped out of college, graduated from high school or dropped out of high school do not have a full time job. The really bad news is that everyone who graduated from college, who dropped out of college, graduated from high school or dropped out of high school from 2007 through 2016 do not have a full time job. There have not been enough full time jobs created in our economy for anyone out of high school or college in the last 9 out of 10 years. If the creation of enough full time jobs to employ only 1 year of college graduates out of 10 years sounds like a tight labor market to you and not a depression, then perhaps some of the readers would like you to share some of whatever you are smoking .

In conclusion, I believe the U.S. economy is in a depression masked by debt. I further believe there is no indication we have had an actual recovery of the actual economy.

These observations could inform intermediate and long term strategies. I am not using these observations as a timing tool, but rather as a depth finder for assessing risk when the next crisis unfolds or when market participants realize the emperor, not only has no clothes, he maxed out his credit cards buying them.